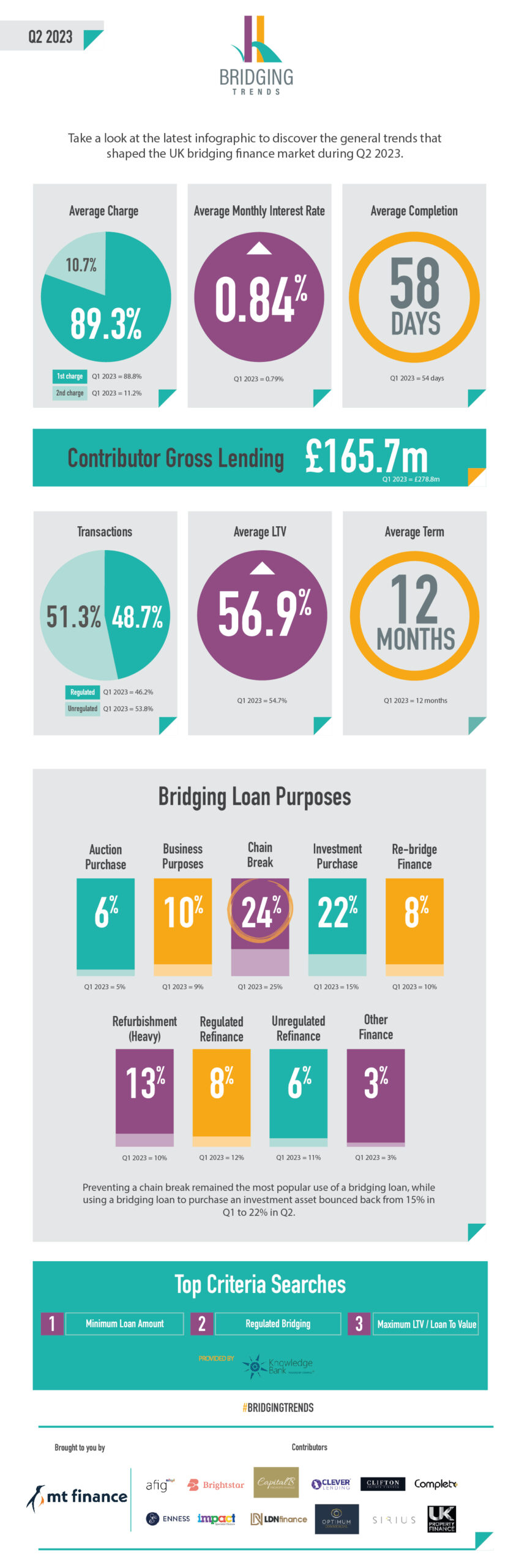

Take a look at the latest infographic to discover the general trends that shaped the UK bridging finance market during Q2 2023

Key Points:

Contributor lending falls 40.6% in Q2

Average monthly interest rate jumps to 3-year high

Investment purchase demand recovers

Demand for regulated bridging increases

Director’s comments

Sam O’Neill, Head of Bridging at Clifton Private Finance, comments:

“The rise in rate doesn’t come as a huge surprise but it’s good to see that it isn’t as much of a dramatic knee-jerk reaction as perhaps it could have been. “Chain break” leading the charge in loan purposes shows that despite cost, a bridging loan is often a means to an end and that the juice is worth the squeeze. Similarly, it’s no surprise to see investment purchases on the rise as investors (new and old) capitalising on opportunities in the marketplace often come to the surface at times of uncertainty.”

Dale Jannels, MD at impact Specialist Finance, comments:

“Although these latest figures might seem gloomy in terms of lending volumes in Q2, it feels far from it in terms of enquiries, although it is definitely harder and more time-consuming to get some cases placed and funded with interest rates where they are currently. Despite this, what we are seeing is more motivated borrowers and fewer ‘tyre kickers’, which leads me to suspect a degree of pent-up demand is there and is ready to be unleashed once economic conditions become more favourable.”

Matthew Dilks, Bridging & Commercial Specialist at Clever Lending, comments:

“I have heard suggestions that regulated bridging will start to reduce as property sale exits are squeezed by lower sale values being achieved, but these figures along with what we are seeing at the start of Q3 show this isn’t really happening yet and I’m not sure it will either going forward. Within the chain break figures listed, I would anticipate a decent proportion of these will be downsizers and such borrowers have substantial equity, so can ride slight reductions in their eventual sale price.

“Finally, it’s also interesting to see a rise in finance for heavy refurbishments and I would expect to see this continue with professional portfolio investors seeking to improve yields with many opting to buy properties and immediately refurb, with many taking advantage with amateur landlords selling up.”