Take a look at the infographic below to see the trends that shaped the bridging finance market in 2020.

Key Points:

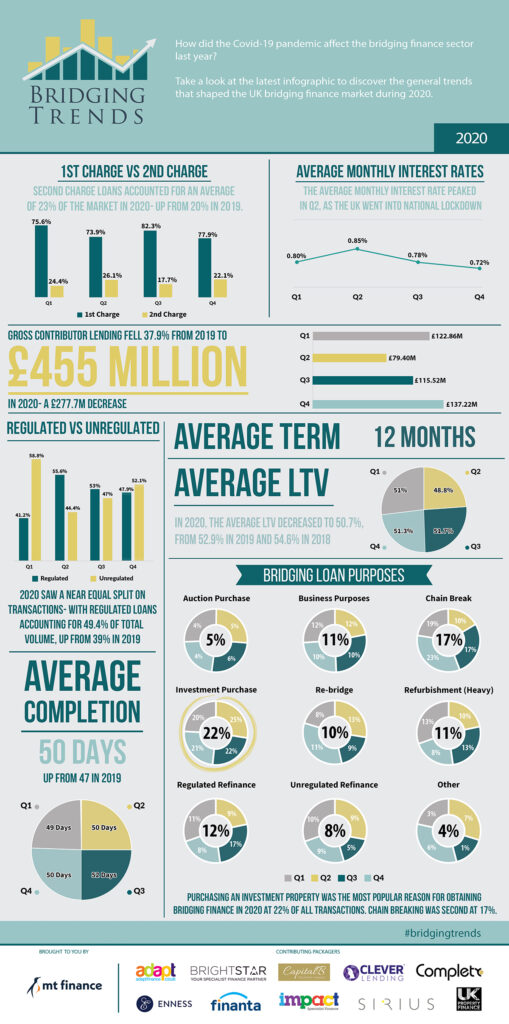

Volume fell £278m in 2020

Interest rates fell to lowest level ever recorded

Average LTV levels decrease to 50%

Near equal split between reg & unreg transactions

Director’s comments

Gareth Lewis, commercial director at MT Finance comments:

“After the first lockdown, we saw the re-emergence of some larger lenders and if you combine this with the stamp duty changes, it is no surprise that there was a stimulus on rates and regulated bridging in the latter part of the year.

“As the vaccine rolls out and we gradually emerge from this lockdown, I believe we will see a new transactional flow from renewed confidence in the economy and businesses re-establishing themselves.”

Dale Jannels, managing director at Impact Specialist Finance comments:

“The impact of the pandemic on the bridging sector is shown clearly in Q4’s data, but it also alludes to the activity we are now experiencing, some of which, but not all, is related to the Stamp Duty Holiday deadline.

“It’s clear though that bridging finance is becoming better understood by the wider broker market (not just those in the specialist sector) and there is more confidence about the options it can provide customers, which should mean that 2021 could see a real watershed moment for this type of finance.”

Kevin Blount, head of operations at Clever Lending comments:

“We certainly had an increase in enquiries during H2 which led to a spike in new business submitted to lenders in Q4. We are working hard with lenders to find solutions, who in turn are reviewing their criteria and interest rates to fit the current market.

“The SDLT holiday as helped to bring business to the bridging market, which is continuing into 2021.”

Chris Whitney, head of specialist lending at Enness comments:

“I am actually quite surprised that the fall in lending quantum in 2020 was so large. The market has always ‘felt busy’ and Enness didn’t see such a big drop in lending volumes.

“Yes, we did see some big names in bridging close their doors as the whole country was forced to work out their strategies in the face of the pandemic on a micro and macro scale, some still aren’t back as they were. However, I think most of the short-term lending market either caried on throughout or paused only temporarily as working practices were refined and made fit for purpose under the restrictions we faced, as well as the level of uncertainty that still hangs over us.

“The absence of some big names reduced supply, coupled with some restricting LTVs, has had a marked impact on lending levels. I think this is also reflected in the fall in average LTVs over the year.

“However, as the trend in Q3 & Q4 indicated, I think we will see volumes bounce back quite quickly and with people re-entering the market the data is reflecting the stiff competition lenders face for business in terms of lower interest rates.

“There are some big high street names who see themselves as ‘business banks’ but I know from first-hand experience that many did not step up to the challenge and support their customers as they should at this time. Borrowers were turned away or faced a huge amount of red tape to navigate on their own and not able to get the support they needed so badly in a timely manner.

“I think this is reflected in the increase in second charge loans and the increase in regulated loans as well. The mainstream high street lenders made it very hard to increase current loans and if they did it was taking much longer than normal. Consequently, I think that is why we see ‘chain breaking’ high on the list for uses of bridge loans. Lots of borrowers use bridge loans as an essential tool on a regular basis but I think we have seen an increase in new to the sector borrowers which has contributed to a shift in some of the historic dynamics.

“I think overall the short-term lending market can be proud of what it managed to achieve in unprecedented times. I know there are an awful lot of people who are very grateful, whose businesses, personal life and families are better for what the industry was able to offer them.

“I am sure 2021 will have its challenges but I feel our industry is ready to take on whatever is thrown at us.”